Revealing My ETF Portfolio For Dividend Income

Listing the ETFs I own primarily for dividend income

Introduction

Investing in ETFs and index funds is what I’ve always recommended to friends and family who aren’t experienced investors. I’ve always found an S&P 500 index fund or ETF to be the safest and easiest investment to make long-term. If someone auto-invests in an S&P 500 index fund or ETF, it requires very little work and investment knowledge and they’ll likely beat the vast majority of hedge funds and actively managed funds over time. Over the last 15 years through June 30th, S&P 500 index funds beat 92% of large-cap funds, according to The Washington Journal.

Index funds and ETFs are similar, however, ETFs trade like stocks, in that they can be bought or sold at any time during a trading day, while mutual funds are only priced at the end of the day. You might see a difference in the returns because different funds have different expense ratios, costs with operating a fund, etc.

For instance, if you had purchased the Vanguard S&P 500 ETF (VOO) which tracks the S&P 500, your return year-to-date would have been 13.84%. Conversely, if you had purchased the Fidelity 500 Index Fund (FXAIX) which also tracks the S&P 500, your return year-to-date would have been 15.61%, so you would have made a little more with the index fund.

I keep separate brokerage accounts for stocks, retirement, ETF investing (which focuses on dividends but also has funds like VOO and QQQ), fixed income (treasuries and CDs), etc. Last month I revealed my stock portfolio (if you missed it, you can read it here). I’ll go through the others in future posts. In this newsletter, I’ll list the positions in my taxable brokerage account at Sofi that focus on ETFs. For this account, in addition to buying safe funds like VOO, I focus on ETFs that provide a dividend for passive income.

A quick reminder that this is not financial advice, just myself sharing my investments, stocks, index fund strategies, what I'm buying, and where I plan to take those investments.

Please subscribe and help spread the word:

Living Off Dividends and Interest

I am currently semi-retired. The vast majority of my income comes from interest from fixed income (treasuries, money market accounts and CDs), which have really great rates right now since interest rates are so high. Since I make enough from those, I reinvest the dividends from my ETFs and stocks. However the interest from the fixed-income investments will (likely) drop at some point, and when that happens, I might shift to have some of my income come from dividends.

My ETF Holdings

I currently own 8 ETFs. I use SoFi for the majority of my ETF investing because their platform lets you auto-invest (similar to Robinhood). Most brokerages allow you to auto-invest in mutual funds and index funds, but not stocks and ETFs. You can auto-invest weekly, every two weeks or monthly. I currently invest weekly.

Below are my ETF holdings as well as their dividend yield, as well as how often the dividends are paid:

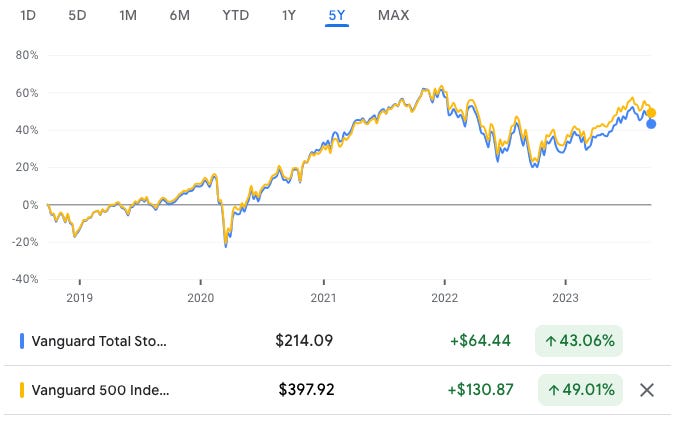

I noted in the newsletter about my stock holdings that in all of my investment accounts, I have an investment that tracks the market that I buy into any time I trade. In this case, I have two, VOO and VTI.

The best thing about investing a fixed amount on a regular basis regardless of the share price (also called dollar cost averaging) is that you can just leave it alone and with VOO and VTI, over time those have always done well regardless of if there is a bad month or year.

Why Both VOO and VTI?

VOO and VTI are very similar. VOO invests in stocks in the S&P 500 Index, which represents the 500 largest U.S. companies. VTI tracks the performance of the CRSP US Total Market Index, which represents approximately 100% of the investable U.S. stock market and includes large-, mid-, small-, and micro-cap stocks regularly traded on the New York Stock Exchange and Nasdaq. If you look at the returns over the past 5 years, they are very similar with VOO edging out VTI by almost 6%.

VTI is my main ETF simply because I have so many investments that track the S&P 500 in my other accounts. The reason I also own VOO is last year in June, I was planning to start a YouTube channel about finance. I thought it would be an interesting experiment to buy VOO and invest weekly and share the performance. So I bought VOO and have continued to invest weekly into it. Although I ultimately did start an investment YouTube channel (which is here), I just realized that creating videos wasn’t my thing. But I will do a future newsletter dedicated to it including how much I initially invested, how much I invest weekly, and how much it is worth now.

Conclusion

Please let me know your thoughts on this newsletter and submit any feedback. You can follow me on Twitter at @TheRajGiri or on Threads at @RealRajGiri . If you haven’t already, please subscribe below:

STWD is not an ETF